Three red days in a row. The ticker is down, your screen is red, and the question is whether tomorrow continues the streak or breaks it. Most traders answer that with feel. The Daily Streaks tool answers it with a literal walk through every consecutive-day streak the ticker has ever printed.

For SPY, that's almost a thousand 2-day red streaks across the historical window. The right question to ask isn't "will it bounce." It's a sharper one: given that the streak has now reached N days, what's the historical probability it stretches to N+1? To N+2? To N+5?

What the tool shows you

Pick a ticker (SPY, QQQ, IWM, AAPL, NVDA, TSLA, PLTR up front; AMD, AMZN, GLD, GOOGL, META, MSFT, NFLX, SLV in the More dropdown). Set Direction to Positive or Negative. Set the Streak Length stepper, or hit Reset to Current Streak to load whatever streak is happening on this ticker right now. Four results cards populate.

The header card tells you how common the streak you're asking about actually is. For "SPY 2-day negative streaks": 965 occurrences · every 9 trading days · last one was 1 trading day ago. That's the baseline frequency: whether you should think of this streak as rare or routine.

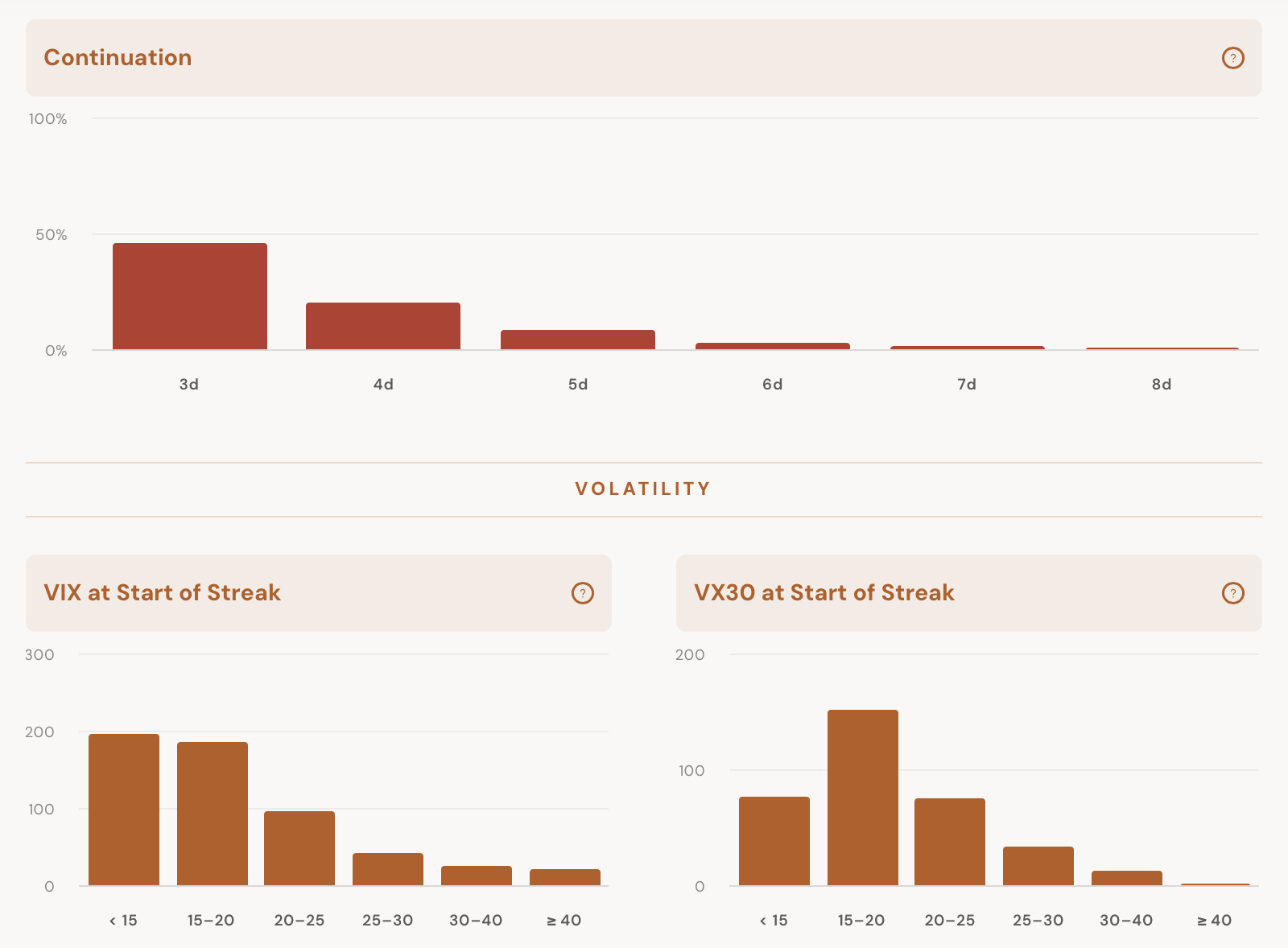

The continuation card is the headline read. It's a stair-step probability: of every 2-day streak that ever happened, 46.0% (443/964) kept going to a 3rd day; 19.1% (184/964) made it to 4 days; 7.2% to 5 days; 2.2% to 6 days; 0.8% to 7; 0.2% to 8. Both numerator and denominator on every row, so you see the actual sample size behind the percentage. That's the real "what happens next" answer: not a forward-return projection, but a clean conditional probability.

The VIX and VX30 at Start of Streak cards show the volatility regime each historical instance started in: a histogram of counts in the <15, 15–20, 20–25, 25–30, 30–40, and ≥40 buckets, plus the average VIX/VX30 across all matches. Lets you check whether the streak you're sitting in is happening in a calm tape (low VIX cluster) or already inside a volatility event.

Below the cards, an expandable event log lists every streak in the ticker's history with date, price at start, VIX at start, VIX at end, and the actual streak length it reached. Useful for sanity-checking the medians or scanning for regime drift. An old streak from 2008 might tell a different story than a 2024 streak even if both fall in the same VIX bucket.

Comments

Loading comments…