Intraday traders argue endlessly about which weekday actually trades clean. Some swear by Monday open-to-close; others say Tuesday is the only day with any reliable directional drift; a handful claim Friday is a graveyard you should sit out. None of them have run the numbers on the ticker they're trading. We did.

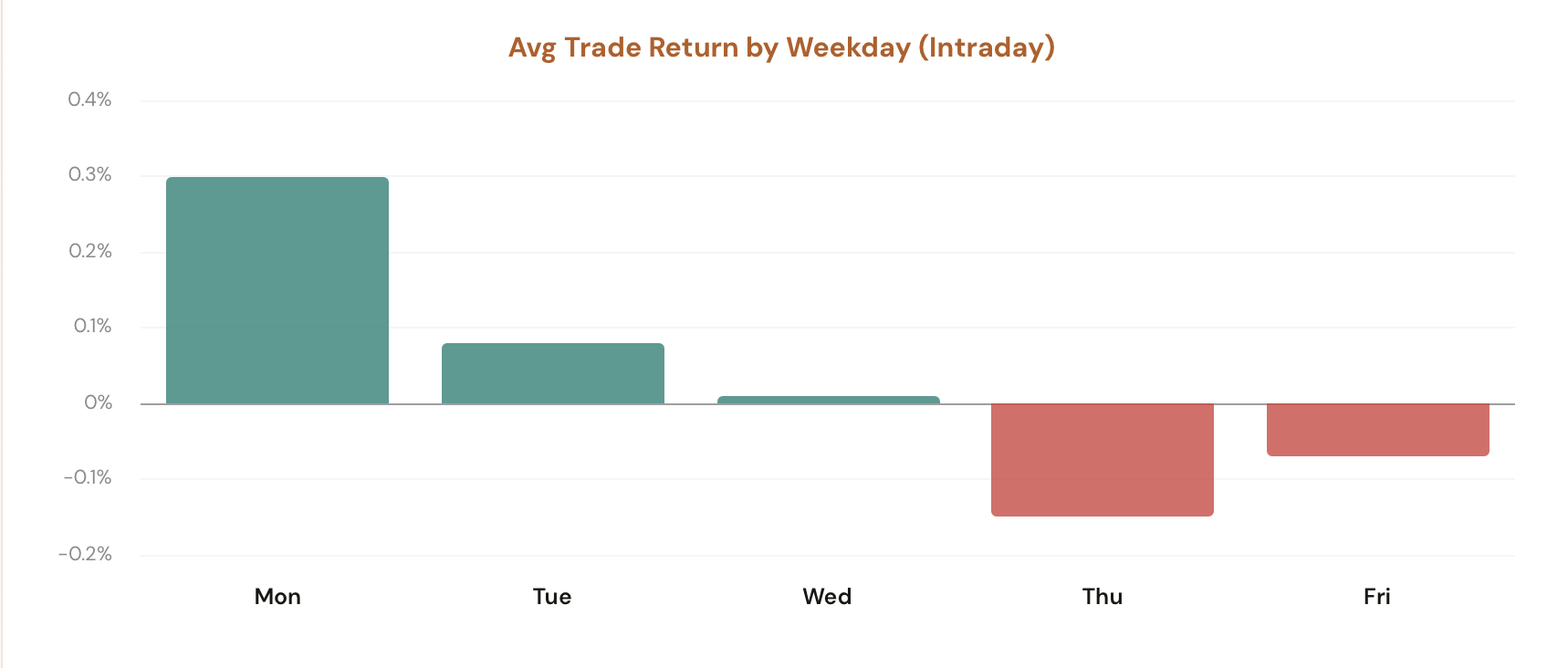

Pick a ticker. Pick a weekday to enter. The tool walks every bar in the historical record, simulates the buy-at-the-open / sell-at-the-same-close trade, and shows you four numbers and a per-trade audit log. A five-bar chart underneath compares the average per-trade return for every weekday side by side, so you can see whether Wednesday's intraday session beats Friday's at a glance.

The Intraday Trading tool answers "which weekday's session pays" without the hand-waving.

The screenshot says it all

Pick a ticker from the pills (SPY, QQQ, IWM, AAPL, NVDA, TSLA, PLTR are pre-loaded; the More dropdown adds AMD, AMZN, GLD, GOOGL, META, MSFT, NFLX, SLV; or type any symbol). The Parameters sidebar gives you three controls: Day (Mon–Fri to choose the entry weekday), VIX Regime (No Filter, <20, 20–30, >30), and Moving Average (No Filter, <5D, >5D).

The main panel returns the four stat cards plus a collapsible trade log listing every individual trade by entry date, entry price, exit date, exit price, and return. Underneath, the Avg Trade Return by Weekday chart breaks the same backtest out across all five weekdays so you can compare which entry day historically held the edge.

Comments

Loading comments…