"Don't buy at the top" is the most-repeated rule in retail finance, and one of the most misleading. Stocks that print new all-time highs have just done the single most bullish thing a chart can do: closed above every prior close in their history. The "buy low, sell high" instinct says wait. The data says it depends, and "depends" is exactly what a backtest is for.

So we built the test. Pick a ticker. Set a profit target. Set a stop loss. The tool walks every bar in the historical record, fires an entry on every day the close prints a fresh all-time high (and the prior bar didn't), exits on whichever happens first (your profit target or stop loss), and shows you the result trade by trade. An equity curve sits next to a buy-and-hold line so you can see whether chasing the top actually beat sitting still.

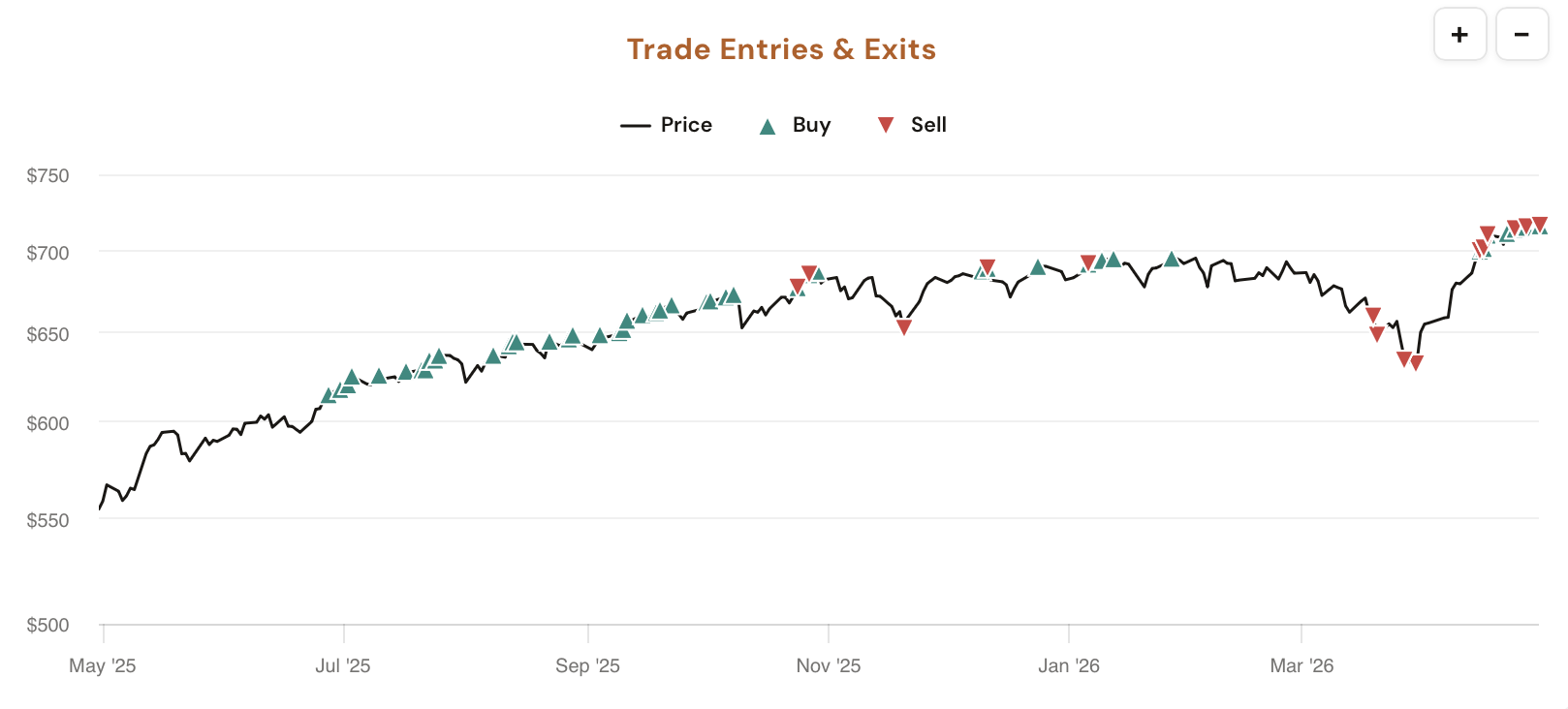

The ATH Backtesting tool is the answer to "does buying all-time highs actually pay" without the proverb-quoting.

Pick a ticker from the pills (SPY, QQQ, IWM, AAPL, NVDA, TSLA, PLTR are pre-loaded; the More dropdown adds AMD, AMZN, GLD, GOOGL, META, MSFT, NFLX, SLV; or type any symbol). The Parameters sidebar gives you two controls: Profit Target (5–50%, default 10%) and Stop Loss (5–50%, default 5%). Entry is fixed: every fresh all-time-high close fires a long on the close.

The main panel returns five stat cards plus a collapsible trade log listing every individual ATH-triggered trade by entry date, entry price, exit date, exit price, days held, exit reason (target or stop), and return. Underneath, an equity curve compounds your strategy's per-trade returns and overlays a buy-and-hold curve on the same ticker, and a Trade Entries & Exits price chart plots every ATH trigger directly on the price line.

Comments

Loading comments…