Every volatility trader has noticed it: certain months feel worse than others. February seems to crush UVXY shorts. Summer feels like a slow bleed. But is any of that real, or is it just selective memory?

Seasonality is one of the most discussed but least measured edges in volatility trading. People talk about "sell in May" or "October volatility" without ever looking at the actual numbers for the specific products they trade.

Until now, getting real seasonality data for leveraged and inverse ETFs meant downloading years of price data and building your own monthly return tables. Most traders never bother.

We built something better.

Introducing the Seasonality Tool

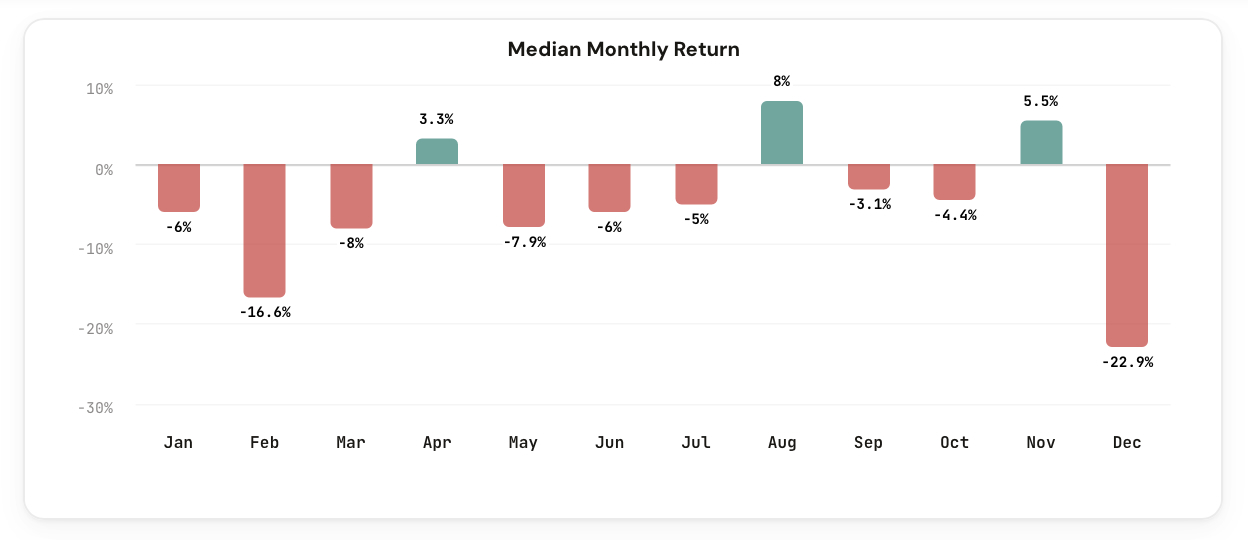

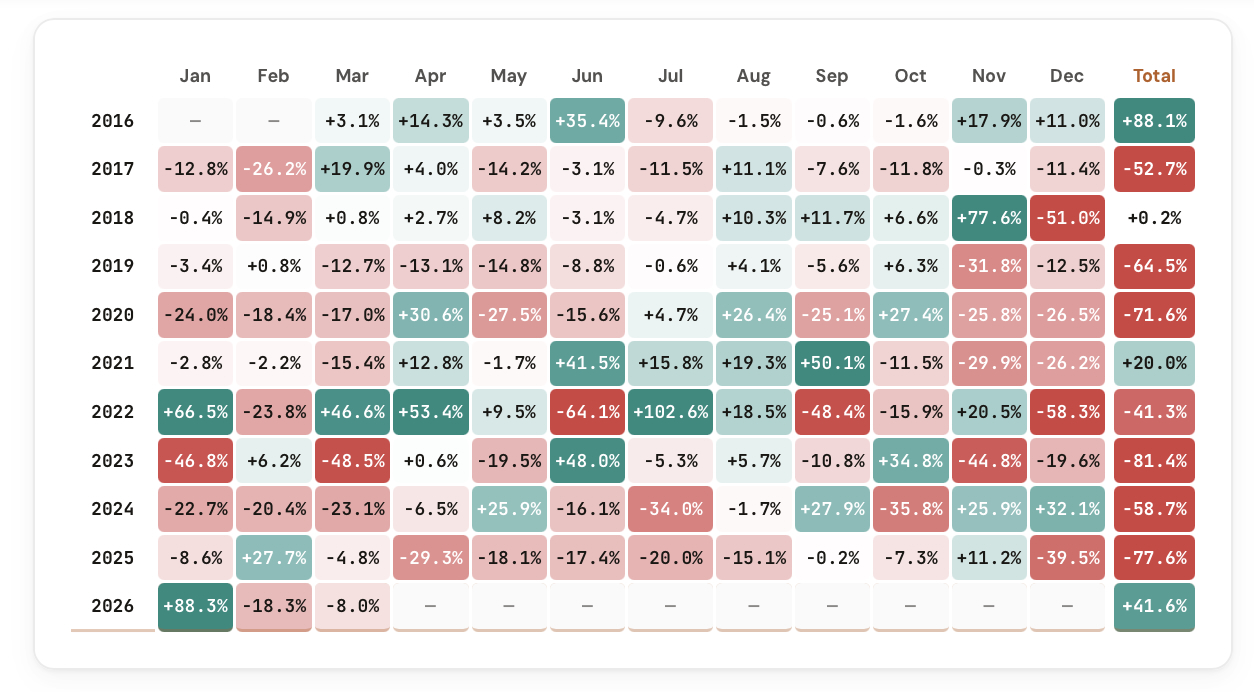

The Seasonality Tool shows monthly return patterns for every ticker in the CI Volatility suite. Pick any product, and you instantly see the median and average return for each month of the year, going back to the full available history.

Select UVXY and you see which months historically delivered the worst losses and which months offered brief reprieves. Switch to SQQQ or SOXS and compare whether the seasonal patterns hold across different leveraged products.

Comments

Loading comments…